Anthropic reported $30 billion in annualised revenue, launched a fully managed agent infrastructure platform, and quietly distributed its most capable model to a restricted group of partners without releasing it to the public. OpenAI’s chief revenue officer responded with a four-page internal memo arguing Anthropic is gaining momentum in enterprise — and separately, Sam Altman confirmed that pre-training for OpenAI’s next frontier model finished on March 24, with a release expected within weeks.

More enterprise customers means more sustained inference load on the same constrained stack. The model race is the demand engine.

What the Revenue Numbers Actually Say

Anthropic said on April 6 that its run-rate revenue had surpassed $30 billion in 2026 — the first time any rival has publicly claimed to match or surpass OpenAI’s run rate of $25 billion. There is a caveat.

OpenAI’s CRO pushed back in an internal memo, first reported by CNBC and later published in full by The Verge, arguing Anthropic’s number is inflated by roughly $8 billion. The accounting difference: Anthropic counts gross revenue from cloud partners, booking the full amount billed through AWS and Google Cloud before those platforms take their cut. OpenAI reports net of Microsoft’s share. Adjusted for that, the real comparison is closer to $22 billion versus $25 billion — OpenAI still ahead.

The accounting dispute matters less than the enterprise momentum in Ramp’s data. In Ramp’s April 15 AI Index update — built from corporate card and bill-pay flows across 50,000+ US businesses — Anthropic reached 30.6% of AI-paying businesses versus OpenAI’s 35.2%, cutting the gap to 4.6 percentage points. That is not a direct measure of token demand, but it is one of the clearest public indicators of enterprise customer momentum. OpenAI’s own CRO considered that momentum serious enough to write a four-page memo.

The revenue composition gap reinforces it. Anthropic’s mix skews heavily toward enterprise — CEO Dario Amodei has cited roughly 80% of revenue from business customers — while OpenAI carries a larger consumer share. Enterprise workloads run longer, burn more tokens per session, and sustain higher memory loads than chatbot interactions. As Anthropic gains enterprise share, the per-customer infrastructure demand rises with it.

What Anthropic Is Not Releasing — and Why

On April 7, Anthropic announced it had built what it described as the most capable model it has ever created. Then it did not release it.

Anthropic’s Project Glasswing gives Mythos Preview to a restricted set of launch partners and additional critical-infrastructure organizations for defensive cybersecurity work, underscoring both the model’s capability and Anthropic’s decision not to release it broadly. Twelve named launch partners — including AWS, Apple, Google, Microsoft, and NVIDIA — received access, alongside more than 40 additional organisations that build or maintain critical software infrastructure.

The benchmark numbers explain the caution. Mythos leads 17 of 18 benchmarks Anthropic measured. On SWE-Bench Verified — real-world software engineering — it scores 93.9%, up from 80.8% for the prior model. A 13-point gain in a domain where 2-3 points was previously considered meaningful progress. On CyberGym, the cybersecurity capability benchmark, it scores 83.1%. In one test, it developed 181 working browser exploits from vulnerabilities it autonomously identified, versus 2 for the prior model.

That last number is the reason for restricted release, stated plainly. The same capability that finds vulnerabilities at scale can be redirected to weaponise them.

The strategic implication is less obvious. Anthropic is holding a capability tier above what is publicly available — deliberately, with named enterprise partners, as a demonstration of safety discipline. This is not just caution. It is positioning. The enterprises deploying AI in regulated, high-stakes environments have a procurement story to tell their boards. Anthropic is building that story one announcement at a time.

Whether Mythos eventually reaches general availability is not confirmed. What the restricted access does establish is a demand signal: when a model at this capability level deploys at broader scale, inference load goes up again. That timeline is unknown, but the direction is not.

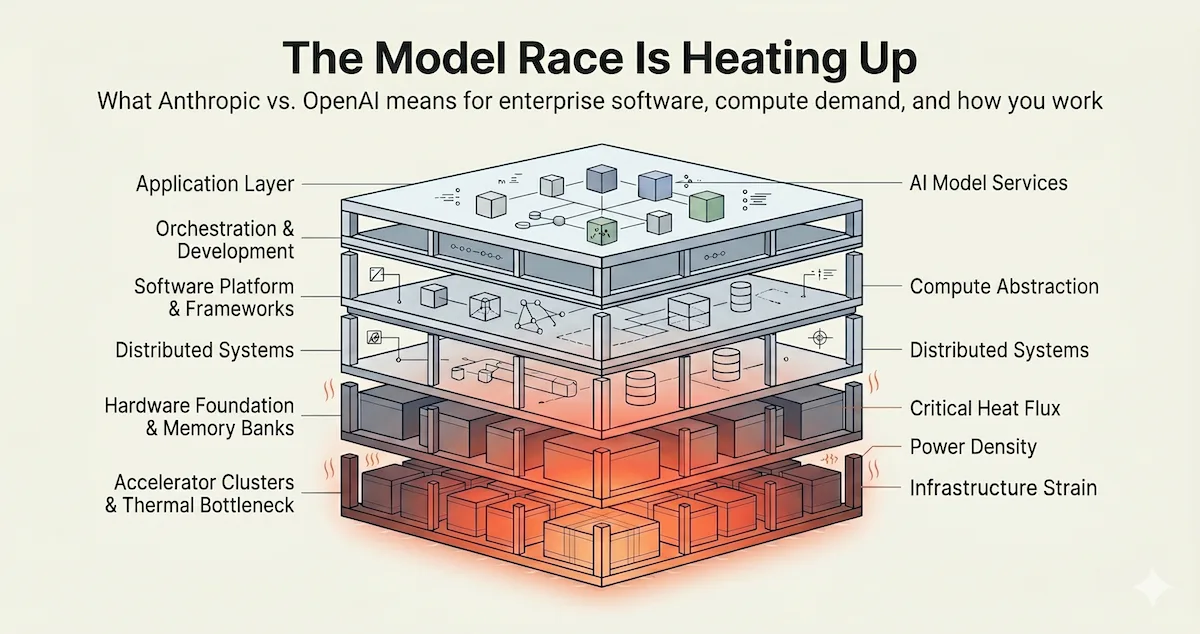

The Inference Supercycle

In 2023, training dominated AI compute. Building the models consumed most of the resources. Running them was secondary.

That has reversed. Inference now accounts for roughly two-thirds of all AI compute in 2026, up from one-third in 2023 and half in 2025, according to Deloitte’s 2026 TMT Predictions report. The shift is structural. Enterprises are not experimenting anymore — they are running AI in production, continuously, at scale.

Claude Managed Agents, launched in public beta on April 8, moves Anthropic further from selling model access alone toward operating agent infrastructure on behalf of customers. Define the agent in natural language or YAML (a configuration file), set the guardrails, and Anthropic handles hosting, scaling, and monitoring. Sessions are persistent. Context is maintained across the full task lifecycle. Runtime is billed at $0.08 per session hour, on top of standard token costs.

What Managed Agents actually represents is a shift in the unit of compute. A chatbot interaction is a round trip — a few seconds, a few thousand tokens, done. A managed agent session working through a codebase or a complex document runs for minutes or hours, consuming 100K to 500K tokens before it finishes. Previously, deploying that kind of session in production required your team to build and operate the infrastructure. Anthropic is now absorbing that entirely. The compute demand per customer goes up. The barrier to creating it just dropped by an order of magnitude.

Jevons paradox is already visible — the idea that making something cheaper and easier to use tends to grow total demand, not shrink it. Managed Agents reduces the fixed engineering cost and operational friction of running an agent workflow. The runtime fee is only part of the bill; the bigger change is that Anthropic is absorbing the sandboxing, orchestration, session management, and monitoring work that previously took teams months to build. When agent infrastructure gets easier to deploy, more companies deploy agents. When more companies deploy agents, total token volume rises. That is the pattern that has defined every prior technology supercycle — efficiency enabling more usage, not less.

What This Means for How You Work

The practitioner shift is already visible in the tooling. Ninety days ago, AI coding tools mostly behaved like assistants: you wrote the prompt, they returned a draft, and you reviewed it. Now the workflow is increasingly supervisory. Tools like Claude Code can break work into subtasks, operate over longer sessions, and come back with code, tests, and follow-up actions. The job is moving from writing better prompts to defining the task, setting constraints, and reviewing the result.

That changes the economics as well as the workflow. A short assistant interaction might use a few thousand tokens; an agentic session working through a real codebase can run far longer and consume materially more compute before it is done. Managed runtimes extend that pattern beyond code into research, operations, and back-office workflows. The human is still in the loop, but later in the process: less step-by-step execution, more specification and review. From the infrastructure side, that means more compute consumed per completed task, not less.

Where Value Accretes in the Stack

The model race has one clear beneficiary at the infrastructure layer: NVIDIA. More inference sessions mean more GPU utilisation. Longer, persistent sessions mean more HBM (high-bandwidth memory) demand per GPU. Neither Anthropic nor OpenAI is building infrastructure that reduces demand for Blackwell or Vera Rubin. They are filling it.

The underlying supply picture hasn’t changed — HBM is sold out through end of 2026, CoWoS (TSMC’s advanced chip packaging) capacity is dominated by NVIDIA reservations, and neither constraint eases because the demand driver changed form. Managed Agents is a new demand signal layered on top of an already constrained stack. Watch for capex guidance in Big Tech earnings starting April 22 — any upward revision in inference infrastructure spend is the first public confirmation of the agent-driven shift.

The more interesting question is what happens in the middle. Enterprise software companies that built their value proposition on “we’ll handle the AI complexity for you” face a different competitive environment when Anthropic is running the agents directly. Notion is an early Managed Agents adopter — which means Notion is now a customer of Anthropic’s infrastructure layer, not just its models. The orchestration, session management, and monitoring that middleware vendors and integration platforms previously sold as differentiation is now a platform feature at $0.08 per hour.

The vertical integration runs in both directions. As the labs move down toward infrastructure, the value of the application layer becomes harder to defend on anything except proprietary data, workflow depth, or distribution. Building on top of a lab that is also building your product’s core infrastructure is a different strategic position than it was eighteen months ago. Companies that assumed the frontier labs would stay in their lane are finding that assumption was wrong.

What Could Break This

The inference demand thesis weakens if efficiency compounds faster than usage.

Managed Agents supports built-in prompt caching, compaction, and other context optimizations. If those systems deliver high cache hit rates or reduce repeated long-context reads, the effective compute footprint per workflow could come in below the raw token math. Anthropic has not published workload composition or realized cache-hit data. Until it does, this is an unknown variable with real weight.

The enterprise crossover story deflates if OpenAI’s push accelerates faster than Anthropic can convert. OpenAI is already at 40% enterprise revenue, up from 30% a year ago, and is not standing still. The Ramp data shows Anthropic momentum, not a completed crossover.

Open-weights models are the structural floor under both. Meta’s Llama 4 supports a ten-million token context window and runs on commodity infrastructure. If open-source frontier models reach enterprise-grade reliability, enterprises running their own inference infrastructure do not add demand to the constrained GPU clusters that Anthropic and OpenAI are filling. They move the load elsewhere — and the managed inference moat both companies are building becomes harder to price above cost.

What We Are Watching

Enterprise customer share crossover. The Ramp AI Index has Anthropic closing fast — from 24.4% to 30.6% in the latest monthly update. The next Ramp release will either confirm the trajectory or show it stalling.

Managed Agents adoption velocity. The list of enterprise names announcing integrations over the next 90 days will indicate whether the managed-runtime model is clearing the market.

Big Tech earnings, starting April 22. TSMC’s Q1 results confirmed 35% revenue growth and CoWoS capacity dominated by NVIDIA reservations. The question for Meta, Google, Microsoft, and Amazon is whether capex guidance reflects agent-driven inference load. Any upward revision in inference infrastructure spend is direct confirmation of the demand signal we are tracking.

Next frontier models: Mythos and Spud. Mythos Preview is now accessible through Amazon Bedrock as a gated research preview — allowlisted organisations, cybersecurity use cases only, US East region. That is a narrower channel than general availability, but it is no longer purely internal. Watch how quickly the allowlist expands and whether use cases beyond cybersecurity get cleared. On the OpenAI side, Spud remains a rumour with no public benchmarks or confirmed release date, despite pre-training completing on March 24. Altman described it as a model that could “really accelerate the economy.” If Spud launches with a step-change in capability, it raises the inference demand ceiling and resets the competitive framing — in both directions.

IPO filings. Anthropic is rumoured for October 2026. The S-1 (IPO prospectus) will resolve the gross versus net revenue question definitively, and will be the first public view of actual token consumption, session economics, and infrastructure cost structure. That filing will contain more useful data about the inference supercycle than any estimate produced before it.

This is part of an ongoing series on AI infrastructure economics. Part 1 covered the full bottleneck sequence — power, packaging, fabs, and EUV. Part 2 covered the memory crunch and the compression wave building against it.

For more on the AI stack and where value flows, visit theupcurious.com.

Sources

Revenue and enterprise share

Anthropic $30B ARR (Google/Broadcom compute partnership announcement, April 2026): https://www.anthropic.com/news/google-broadcom-partnership-compute

OpenAI CRO internal memo: The Verge — https://www.theverge.com/ai-artificial-intelligence/911118/openai-memo-cro-ai-competition-anthropic

Ramp AI Index April 2026 — “As AI adoption crosses 50%, the tokenmaxxing economy splits off and up” (Anthropic 30.6% / OpenAI 35.2%): https://ramp.com/leading-indicators/the-tokenmaxxing-economy-splits-off-and-up

Mythos and Project Glasswing

Project Glasswing launch (April 7, 2026): https://www.anthropic.com/glasswing

Mythos Preview benchmarks and technical write-up: https://red.anthropic.com/2026/mythos-preview/

Mythos Preview on Amazon Bedrock (gated research preview): https://aws.amazon.com/about-aws/whats-new/2026/04/amazon-bedrock-claude-mythos/

OpenAI Spud

Leaked memo and Altman pre-training confirmation: https://the-decoder.com/openais-leaked-memo-says-new-spud-model-will-make-all-its-products-significantly-better/

Inference supercycle

Inference = 2/3 of AI compute: Deloitte 2026 TMT Predictions — https://www.deloitte.com/us/en/insights/industry/technology/technology-media-and-telecom-predictions/2026/compute-power-ai.html

Computerworld CES 2026 supporting coverage: https://www.computerworld.com/article/4114579/ces-2026-ai-compute-sees-a-shift-from-training-to-inference.html

Claude Managed Agents overview: https://platform.claude.com/docs/en/managed-agents/overview

Claude Managed Agents pricing: https://platform.claude.com/docs/en/about-claude/pricing

Infrastructure

SK Hynix HBM sold out through 2026: https://www.techspot.com/news/110058-sk-hynix-completely-sells-out-semiconductor-supply-ai.html

Micron HBM sell-out confirmation: https://www.trendforce.com/news/2025/08/13/news-hbm-battle-heats-up-micron-reportedly-hints-2026-sell-out-sk-hynix-yet-to-confirm/

TSMC CoWoS / NVIDIA capacity dominance: https://www.digitimes.com/news/a20260410VL204/packaging-capacity-tsmc-nvidia-demand.html