Big Tech just reported another quarter of record AI spending. The CEO of Google DeepMind said the current approach is probably missing one or two big ideas. And memory suppliers posted record profits that confirm both stories at the component level.

All three signals point in the same direction: AI works, the money is flowing, and the system is still substituting scale for structure.

1. Big Tech Earnings: The AI Bill Keeps Going Up

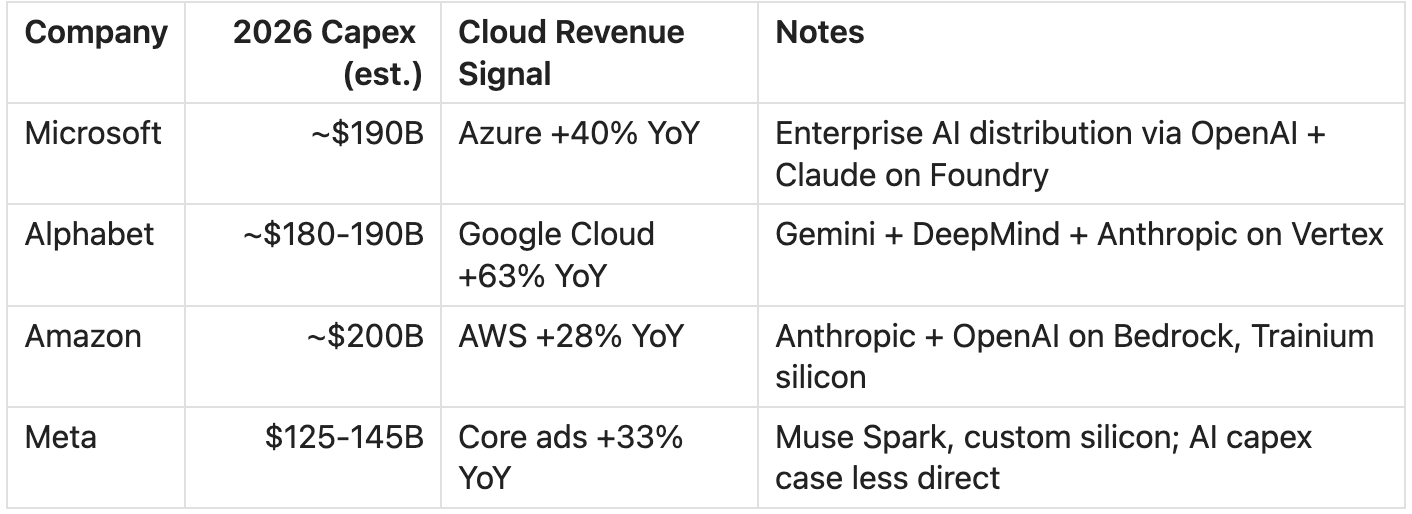

AI is showing up in revenue. Google Cloud had the clearest print, with reported growth above 60% year-over-year. AWS and Azure also showed continued demand. This is the strongest part of the bull case: AI is driving cloud usage, enterprise contracts, model distribution, ad products, and developer workflows.

But the capex bill keeps rising. Microsoft, Alphabet, Meta, and Amazon are now tracking hundreds of billions of dollars in annual spending, with several reports putting combined 2026 capex in the $650-725B range. Every time investors ask when spending normalizes, the hyperscalers raise the number again.

The pattern is clear: companies with direct cloud pull-through are printing revenue while companies waiting for future AI products are asking for patience.

Google Cloud and AWS growth are especially supportive of the AI revenue case because both are now distribution platforms for frontier models, not just raw compute sellers. Microsoft is still the deepest enterprise AI distribution story, but it is no longer only an OpenAI story, Claude is available through Microsoft Foundry, and the Copilot ecosystem spans GitHub, Office, and Azure.

The companies with cloud pull-through look stronger than the ones asking investors to trust future AI products.

The clean read: AI is not failing. The business model is becoming more capital intensive.

2. We Are Still Brute-Forcing Intelligence

This is where Demis Hassabis’s comments become essential context.

Hassabis is the CEO of Google DeepMind, the lab behind AlphaGo, AlphaFold, and Gemini. He is one of the few people who can talk about AGI from both sides: frontier model scaling and scientific AI systems that already solved narrow but extremely hard problems.

He is not dismissing today’s models. DeepMind helped define the scaling path that produced them. Hassabis still thinks the core ingredients matter: large-scale pre-training, reinforcement learning, chain-of-thought style reasoning, and tool use. He does not think this path is a dead end.

But he also thinks the final AGI architecture might still be missing one or two big ideas. His framing is closer to 50/50: maybe existing techniques scale with incremental innovation, maybe one or two new ideas still need to be cracked.

The gaps he points to change the compute math.

Continual learning. Current models do not naturally learn from the environments they are deployed into. They can use retrieval, logs, files, and memory features, but the model itself is not gracefully updating from lived experience.

Long-term reasoning and self-monitoring. Models can solve very hard problems and still fail simpler variants. The missing layer is not just “think longer.” It is monitoring the thinking itself: noticing when a reasoning chain is looping, going off-track, or returning to a known bad answer.

Episodic memory. A million-token context window is useful. It is also a crude memory system. Throwing everything into context is not memory. It is hoarding.

These are not abstract research gaps. If memory systems improve, agent sessions get shorter and cheaper — fewer tokens burned per task, less brute-force context stuffing. If they stay crude, every session scales linearly with task count, and the inference bill climbs with it. Which path we land on determines whether the current capex trajectory is a peak or a floor.

He also points in the other direction: edge compute, efficiency, and smaller models. The future is not only bigger frontier models in larger data centers. It is also capable local models running on phones, glasses, robots, laptops, and enterprise devices, handling private or low-latency work locally and sending only the hardest tasks back to the cloud.

The current path works like this:

Need more knowledge? Add context.

Need better answers? Add reasoning tokens.

Need more autonomy? Add an agent loop.

Need reliability? Add retries, verifiers, and human review.

This works. But it is expensive and incomplete. A system can be economically huge before it is AGI.

The risk to the brute-force framing is not that AI stops improving. It is that intelligence gets cheaper, smaller, and more distributed. That would not be bad for AI. It would rotate the winners.

3. Memory Earnings Confirm the Compute Crunch

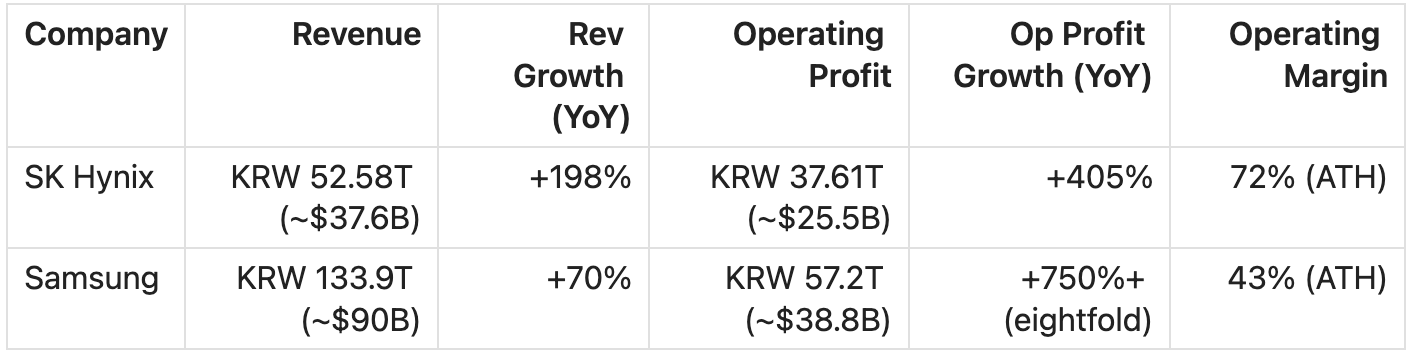

If Big Tech capex is the top-down view of AI demand and Hassabis’s critique is the intellectual frame, memory supplier earnings are the bottom-up confirmation. Both Korean majors posted record quarters within days of each other.

The numbers tell the demand story. What they don’t tell is the supply story. SK Hynix says demand will outpace supply for at least the next three years and customers are prioritizing volume over price. Samsung’s semiconductor (DS) division is operating above 70% margins, but consumer electronics and display drag the blended company margin to 43%. The chip business now accounts for more than 90% of total Samsung earnings. Both companies say the supply-demand gap will widen further in 2027.

This is the compute thesis playing out at the component level. Every agent session, every reasoning chain, every context window needs HBM. The bottleneck is not just GPUs. It is the memory that feeds them.

Micron (MU) is the third-largest HBM supplier and the clearest Western beneficiary of a supply-constrained memory cycle that both Korean majors say has years left to run.

Investment Read

The obvious trade is NVDA. The less obvious question is what the market is still underpricing.

The memory debate is about duration, not demand. Nobody doubts memory is hot, Samsung is up 114% YTD, SK Hynix has roughly tripled since August. The real question is whether the market is right to price these as peak cyclical margins. Samsung trades at 5.78x forward earnings. That says: “these earnings don’t persist.” Both companies say supply is committed through 2028 and the gap widens in 2027. If they’re right, the multiple is wrong, not because demand is in question, but because the cycle has longer legs than the market expects. MU is the cleanest US-listed expression; DRAM (Roundhill Memory ETF, launched April 2026) gives 27% SK Hynix, 23% Samsung, 21% Micron in one ticket.

Cloud is the distribution story, not the compute story. Google Cloud at +63% and AWS at +28% are not just selling GPUs. They are the procurement layer, the enterprise channel through which every frontier model reaches production. GOOGL is the most interesting here: Gemini, DeepMind, TPUs, Anthropic on Vertex, and Google Cloud growing faster than the other two. The market still prices it as a search company.

The risk nobody is talking about: winners rotate. If memory systems improve, models get smaller, edge inference scales, then the current winners (GPU makers, memory suppliers, cloud infrastructure) face a world where intelligence gets cheaper and more distributed. That does not kill AI demand. It rotates the beneficiaries toward device makers (AAPL, QCOM, ARM), model efficiency companies, and anyone owning the workflow layer. The application layer is the riskiest place to be if you own a prompt wrapper, and the most valuable place if you own the workflow.

What To Watch

Cloud revenue versus capex. Microsoft, Alphabet, Meta, and Amazon are tracking $650-725B in combined 2026 capex. If any two report revenue deceleration in the same quarter while spending holds, the “capital cycle outrunning revenue” thesis gets real.

Agentic demand. Anthropic and OpenAI ARR are the top-line signals, but the cleaner read is how that revenue is being generated. Watch ARR growth alongside usage-limit changes, enterprise pricing, API rate-limit expansion, coding-agent packaging, and cloud capacity deals. If ARR keeps rising while limits expand and pricing shifts toward heavier usage, the inference load story is intact.

Model architecture. Watch whether frontier labs move beyond larger context windows toward better memory, routing, self-monitoring, and small-model distillation. This is the Hassabis gap. The first lab to ship it well changes the compute math.

Advanced small models. Watch Qwen’s 27B and 35B models, Gemma 4’s 26B MoE and edge variants, and other mini reasoning models. The question is not whether they beat frontier systems outright. It is whether they become good enough for coding, local agents, and enterprise workflows at a fraction of the serving cost.

Memory supply additions. New Samsung and SK Hynix fabs won’t ramp before H2 2027. Micron’s Idaho facility starts mid-2027. If any of these timelines accelerate, pricing pressure arrives earlier than expected.

SK Hynix ADR listing. Expected within 2026. Watch for index inclusion, passive fund inflows, and whether the valuation gap with Micron narrows.

The question is not whether AI keeps improving. It is whether the current architecture is a peak or a floor. The earnings say floor. The memory suppliers say floor. Hassabis says maybe not.

The missing pieces — memory, learning, self-correction — are not just theory. They change which companies win and how much capital the industry burns getting there.